Many in the US banking industry are likely glad to see the back of 2023. The year began with a bust, with some high-profile institutions going into liquidation in the first quarter, and the S&P 500 Financial sector shedding over 20% of its market capitalization by the middle of March.

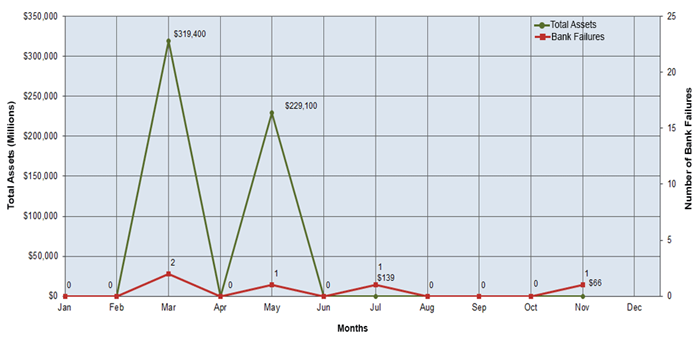

Things started to look up in the second half of the year as interest rates stabilized and valuations recovered in the fourth quarter. However, the failure in November of Citizens First Sac, a bank with $66 million in deposits, showed that smaller institutions were not immune to the contagion. Community lenders are the bedrock of US banking, so it is not surprising that the event prompted nervous discussions about the overall health of the sector.

In this blog post, I’ll explore the significance of this event within the context of the broader banking landscape. Despite concerns about the sky falling on American banks, I’ll argue that such isolated incidents are not indicative of systemic danger but rather a testament to the robustness of the regulatory framework in place.

Survival-of-the-Fittest in banking

Bank failures are an inherent part of the survival-of-the-fittest dynamic within the U.S. banking sector. The system is designed to allow weak banks to fail while safeguarding the vast majority of depositors. The twin backstops of systemically important financial institutions and federal lenders of last resort provide a safety net for the financial system. When a bank like Citizens First Sac experiences a smooth transfer of ownership, as seen with its acquisition by Iowa Trust over a weekend, it validates the effectiveness of the system’s checks and balances.

Historical perspective

Taking a historical perspective, Pew Research reveals that, outside of major crises like the 80s Savings and Loan (S&L) collapse and the 2000s financial crisis, bank failures have averaged just over five per year. The recent failure of Citizens First Sac brings the total to five for 2023, aligning with historical norms. This consistency underscores the system’s ability to manage and absorb the failures of individual banks without triggering systemic risks.

The need to stay vigilant

While the number of bank failures may be within historical averages, it is crucial not to become complacent. Some high-profile institutions faced bankruptcy in 2023, endangering over $300 billion in assets – the third-largest bank run since 1940. This emphasizes that it’s not just the frequency of failures that matters, but also the scale. Thus, banks and regulators must remain vigilant, addressing issues such as poor lending practices, lackluster risk management, and insufficient balance sheet discipline.

The role of real-time payments and ISO 20022

In this context, the role of payments technology, particularly real-time payments services like FedNow and TCH RTP, and the ISO 20022 messaging standard, comes to the forefront. Real-time payments, when coupled with ISO 20022 messaging, offer immediate 24×7 funds transfer with a wealth of embedded data in each transaction.

It’s essential to note that these technologies won’t prevent banks from failing, as institutions with weak fundamentals are bound to face consequences. However, they do empower consumers and businesses by providing greater control over their funds. Additionally, the introduction of real-time payments and the adoption of ISO 20022 create an opportunity for financial businesses to evolve past their weaker peers by delivering higher quality payment services.

Consumers and businesses, armed with the ability to control their funds in real-time, will naturally gravitate towards institutions that offer superior payment services. This paradigm shift represents the latest chapter in the survival-of-the-fittest narrative, where adaptability to technological advancements becomes a key factor in a bank’s longevity.

Conclusion

The failure of Citizens First Sac, when viewed in the broader context of U.S. banking history, highlights the resilience of the system, not its weakness. Bank failures are a natural occurrence, and the regulatory framework in place is adept at handling them without jeopardizing the entire financial sector. Real-time payments and the ISO 20022 standard add a new dimension to this landscape, offering both consumers and institutions an opportunity to thrive in an era where adaptability to technological advancements is paramount. The sky is not falling on American banks; rather, they are evolving