When talking to banks around the world about ISO 20022, several questions and statements arise regularly. There are those who question the need to move to an ISO 20022-based standard, with banks doubting the need or benefits to migrate. On the other hand, there are banks (admittedly, a much smaller number of banks) that are embracing the move to ISO 20022 and are seeking to learn from those who have already done so. These banks usually assume that Europe, having adopted ISO 20022 for SEPA payments more than a decade ago, would find the move to ISO 20022 for SWIFT and Wires easy, and look to them for advice.

European banks, however, will quickly tell you that this is far from the case and that they are struggling.

So where is the European banking industry in their migration? What approaches have the banks taken? And more importantly, will every bank make the deadline?

It is often assumed by non-Europeans that European banks are universally using ISO 20022, yet that is not the case. SEPA applies to specific payment types, and only in the Eurozone. Instead, the story is much more complex. Furthermore, in messaging terms, ISO 20022 is still new, as the standards they are replacing are more than 40 years old.

The industry as a critical point in their migration to ISO 20022. Deadlines are looming, and while banks will always push for extensions, the industry does need to prepare for what may happen next. “Hope for the best, plan for the worst” may seem trite when considering single transactions can exceed €1 billion, but unless the industry takes stock, it is impossible for the industry or banks to even decide what the plan needs to address. Given the impact of the pandemic, banks also need to re-examine their own initial plans and assumptions.

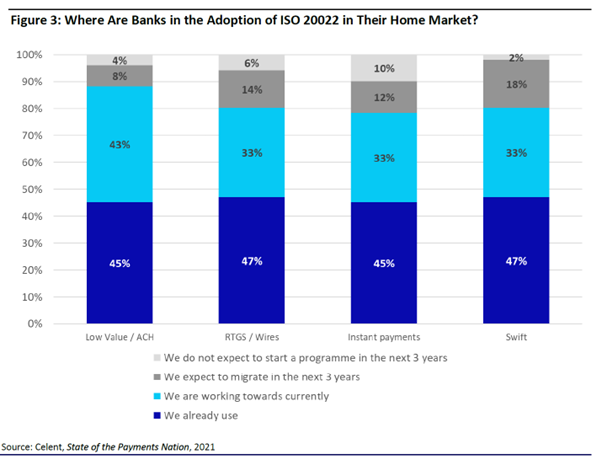

The ISO 20022 messaging standard continues to gain momentum as more and more clearing and settlement mechanisms adopt the new ISO 20022 standard.

Just like in the natural world, the secret to surviving evolutionary pressures is rapid adaptation. That is why payments modernization is so necessary: by gaining the freedom to evolve past their legacy payments technology infrastructures, banks can accelerate the modernization of their payments businesses. Institutions that take the right approach will be ideally positioned to win the “survival of the fittest” race and increase their market share; those that do not will be relegated to irrelevance or extinction.

To better understand where banks are in their moves to ISO 20022, and how to best assess implications of ISO 20022 migration, download your copy of the report.